The Capital Drain: How Policy Uncertainty Weakens Catastrophe Insurance Markets

October 2024

Don D. Brown

P.O. Box 866

DeFuniak Springs, FL 32435

www.dondbrown.com

Table of Contents

The Capital Drain: How Policy Uncertainty Weakens Catastrophe Insurance Markets

Abstract

1. Introduction: Risk and Uncertainty in Catastrophe Insurance Markets

2. Knight's Theory of Risk and Uncertainty

2.1 The Knightian Distinction

2.2 Application to Catastrophe Insurance

2.3 The Economic Implications of Uncertainty

3. The Spectrum from Risk to Uncertainty: A Visual Framework

3.1 Visual Representation of the Spectrum

3.2 Capital Response and the Risk-Adjusted Dial

3.2.1 Tying Together the Risk-Uncertainty Spectrum and Capital Flight

3.3 Factors Influencing Spectrum Position

3.4 Practical Illustration: The Journey from Stability to Volatility

3.5 Implications for Policymakers

3.5.1 Policy Assessment and Impact Analysis

3.5.2 Gradual Implementation Strategies

3.5.3 Balancing Act: Consumer Protection and Market Stability

3.5.4 Communication and Transparency

3.5.5 Fostering Innovation and Market-Based Solutions

3.5.6 International Coordination

3.5.7 Continuous Learning and Adaptation

4. Policy Decisions and Unintended Consequences: A Case Study of Hurricane Insurance in Florida

4.1 Policy Goals vs. Market Realities

4.1.2 Legislative Interventions in Claims Processes

4.1.3 Mandated Coverage Expansions

4.2 Case Study: Florida's Hurricane Insurance Regulation

4.2.1 Historical Context

4.2.2 Key Policy Interventions

4.2.3 Initial Impact

4.2.4 Long-Term Consequences

4.3 Illustration of Risk-Adjusted Spectrum in Policy Context

4.4 Broader Comparisons and Lessons Learned

4.4.1 Healthcare Markets

4.4.2 Energy Markets

4.4.3 Lessons for Policymakers

5. The Economic Consequence of Increasing Uncertainty

5.1 Capital Flight Dynamics

5.1.1 Mechanisms of Capital Flight

5.1.2 Impact on Market Capacity

5.2 Direct Impact on Policyholders

5.2.1 Premium Increases

5.2.2 Reduced Coverage Options

5.2.3 Increased Vulnerability

5.3 Long-Term Market Instability

5.4 Analogy: The "Concert Effect"

5.5 Quantifying the Impact

5.5.1 Insurance Penetration Rates

5.5.2 Premium-to-Coverage Ratios

5.5.3 Market Concentration Indices

5.5.4 Reinsurance Costs

5.5.5 Investment in Catastrophe Bonds

5.5.6 Litigation Rates

5.5.7 Time to Market Recovery

5.5.8 Challenges in Quantification

5.5.9 Future Research Directions

6. Policy Recommendations: Reducing Uncertainty for Capital Stability

6.1 Adopt Predictable Regulatory Frameworks

6.2 Engage with Industry Experts and Stakeholders

6.3 Implement Graduated Adjustments

6.4 Foster Market-Based Solutions

6.5 Enhance Data Collection and Analysis

6.6 Maintain Flexible Capital Requirements

6.7 Enhance Consumer Education and Protection

6.8 Examples of Effective Regulatory Policies

6.8.1 Florida's Post-2005 Reforms

6.8.2 California Earthquake Authority (CEA)

6.8.3 United Kingdom's Flood Re Program

7. Conclusion: The Case for Risk-Adjusted Policies

Key findings from this analysis include:

References

The Capital Drain: How Policy Uncertainty Weakens Catastrophe Insurance Markets

Abstract

This paper examines the dynamics of capital flow in catastrophe insurance markets, focusing on the consequences of policy decisions that shift the market from risk to uncertainty. Drawing on Dr. Frank H. Knight's seminal work on risk and uncertainty, as well as insights from Don Brown's "The 9 Guideline Principles to Enact Change: A Legislator's Memoir – From Outhouse to State House," the discussion explores how poorly considered regulatory changes drive capital flight, destabilize markets, and, paradoxically, reduce consumer protections. By analyzing historical cases, including policy interventions in Florida's hurricane insurance market, the paper demonstrates the critical need for well-informed policies that balance market stability with consumer protection. The study introduces a novel risk-uncertainty spectrum to visualize the impact of policy decisions on market stability and capital availability, providing policymakers with a tool to assess the potential consequences of their actions.

1. Introduction: Risk and Uncertainty in Catastrophe Insurance Markets

Catastrophe insurance, which supports regions prone to hurricanes, earthquakes, and other natural disasters, requires a predictable capital inflow to ensure market stability. Insurers and capital providers rely on stable, manageable risks to sustain these markets. However, policy interventions that increase market uncertainty can drive capital away, reducing the availability and affordability of coverage just when it is most needed.

The delicate balance between risk and uncertainty in catastrophe insurance markets is particularly evident in regions like Florida, where the threat of hurricanes looms large. As Don Brown notes in his memoir, "Florida represents the peak catastrophe risk in the world," making it a critical case study for understanding the interplay between policy decisions and market stability[1]. This unique position amplifies the importance of well-crafted policies that maintain a balance fostering capital retention while protecting consumers.

This paper builds upon Dr. Frank H. Knight's theories on risk and uncertainty to analyze the impact of policy decisions on catastrophe insurance markets. By examining historical cases and introducing a novel risk-uncertainty spectrum, we aim to provide policymakers with a framework for understanding the potential consequences of their actions on market stability and capital availability.

The objectives of this paper are threefold:

To elucidate the distinction between risk and uncertainty in the context of catastrophe insurance markets, drawing on Knight's seminal work and contemporary applications.

To introduce and explain a visual framework—the risk-uncertainty spectrum—that illustrates the relationship between policy decisions, market stability, and capital availability.

To analyze case studies, particularly focusing on Florida's hurricane insurance market, to demonstrate the real-world implications of policy-driven uncertainty on capital flow and market stability.

By achieving these objectives, this paper seeks to contribute to the ongoing dialogue on effective regulation of catastrophe insurance markets, emphasizing the need for policies that balance consumer protection with market stability.

2. Knight's Theory of Risk and Uncertainty

2.1 The Knightian Distinction

Dr. Frank H. Knight's seminal work, "Risk, Uncertainty, and Profit" (1921), introduced a crucial distinction between risk and uncertainty that has profound implications for understanding capital behavior in modern markets[2]. Knight's theory argues that:

Risk represents situations where outcomes, while unknown, have measurable probabilities. These probabilities allow insurers and capital providers to forecast returns and offer coverage accordingly. Catastrophe insurers, for instance, can assess average hurricane damage based on decades of data, making risk calculable and allowing them to set premiums accordingly.

Uncertainty describes scenarios with unknown and unmeasurable outcomes, rendering predictions futile. For example, when policymakers change insurance laws without fully understanding the financial implications, insurers cannot reliably estimate costs, and investors cannot predict returns, resulting in uncertainty.

Knight suggests that uncertainty leads to economic retreat as capital flows away from uninsurable risks to more predictable sectors. This distinction is crucial for catastrophe insurance markets, where predictability determines capital availability and consumer access to affordable coverage.

2.2 Application to Catastrophe Insurance

In the context of catastrophe insurance, Knight's distinction becomes particularly salient. Natural disasters, while inherently unpredictable in their specific occurrences, have historically provided enough data for insurers to calculate probabilities and set premiums accordingly. This falls under Knight's concept of risk—a situation where probabilities can be assigned to potential outcomes.

However, when policy interventions introduce elements that cannot be quantified or predicted, such as sudden changes in claims processes or arbitrary caps on premium increases, the market shifts towards Knightian uncertainty. In these situations, insurers and capital providers find themselves unable to reliably assess their potential returns or losses, leading to market instability and potential capital flight.

As Brown observes in his memoir, "Political uncertainty appears to be the 'weak link' when considering capital investment by insurance and reinsurance companies in Florida"[3]. This observation aligns closely with Knight's theory, highlighting how policy-driven uncertainty can have a more significant impact on market stability than the inherent risks associated with natural disasters.

Real-World Example: Hurricane Insurance in Florida

· Risk: In Florida, hurricanes are a known annual threat. Insurers use historical data, weather patterns, and advanced modeling to calculate the probability of hurricanes, setting premiums based on the risk of storm-related damage. This predictable, measurable approach defines risk—where probability distributions are known.

· Uncertainty: Now imagine if sudden, unpredictable changes in Florida’s insurance regulations create limitations on premium increases or cap payouts. This regulatory uncertainty disrupts insurers’ ability to forecast profits, adding a new layer of unpredictability. Even with historical weather data, insurers face uncertainty because future policy decisions are unknown and unquantifiable, making it difficult for them to ensure sustainable coverage.

2.3 The Economic Implications of Uncertainty

Knight's analysis shows that as uncertainty rises, capital becomes scarce, and costs increase, leaving consumers vulnerable. This principle has been echoed in recent economic literature and validated through practical applications in various markets, including finance and insurance[4].

In catastrophe insurance markets, the shift from risk to uncertainty can manifest in several ways:

Reduced Capital Inflow: As uncertainty increases, investors become more hesitant to commit capital to the market, leading to reduced capacity for insurers to underwrite policies.

Higher Premiums: With less capital available and increased uncertainty, insurers may need to charge higher premiums to cover potential losses, making coverage less affordable for consumers.

Market Concentration: Smaller insurers may be forced out of the market due to increased uncertainty, leading to a concentration of larger insurers and potentially reducing competition and consumer choice.

Coverage Gaps: In extreme cases, insurers may withdraw from certain high-risk areas entirely, leaving residents without access to necessary coverage.

Understanding these implications is crucial for policymakers seeking to maintain stable and effective catastrophe insurance markets. As we will explore in subsequent sections, policies that inadvertently increase uncertainty can have far-reaching consequences that undermine their intended goals of consumer protection and market stability.

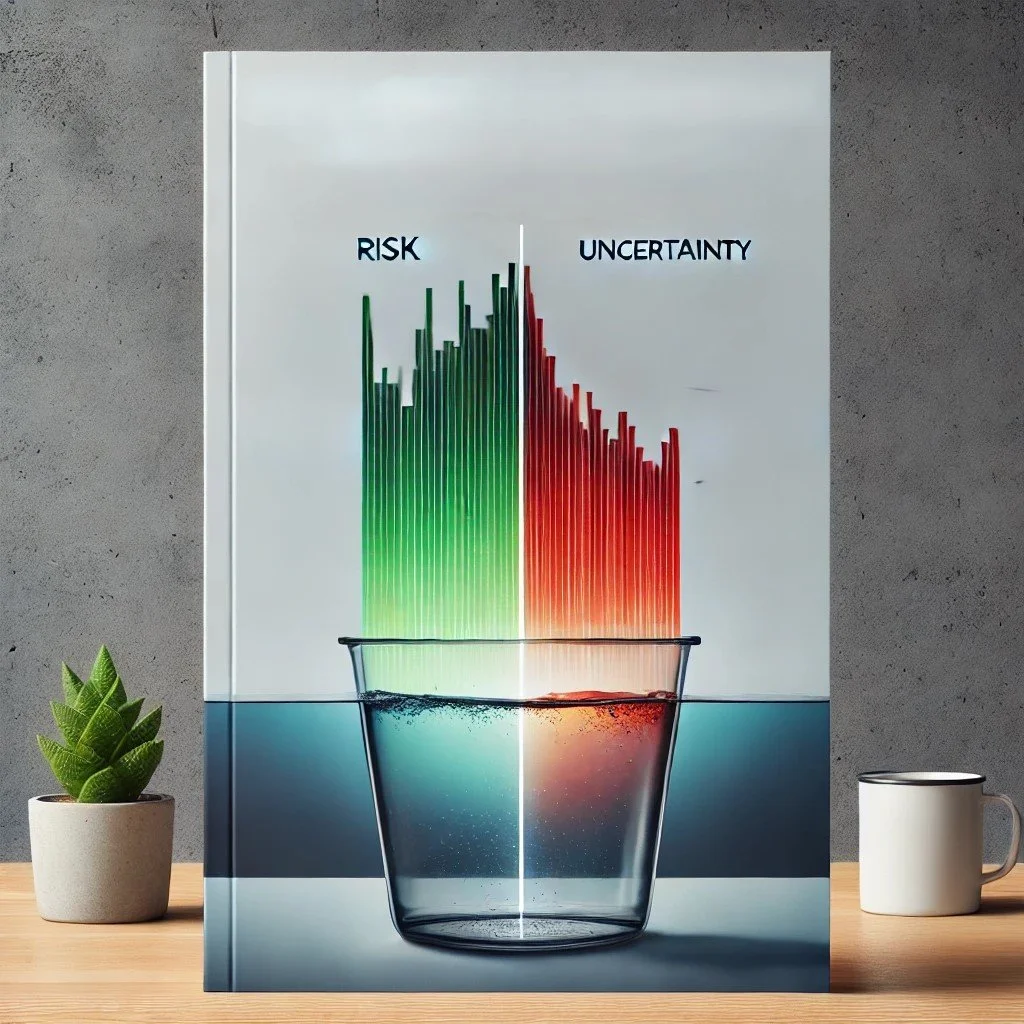

3. The Spectrum from Risk to Uncertainty: A Visual Framework

In catastrophe insurance markets, the stability and availability of capital hinge on the degree of predictability in policy and risk assessment. To clarify how various policy interventions influence market dynamics, we introduce the Risk-Uncertainty Spectrum. This framework visually represents the continuum from a market environment defined by risk—where probabilities are measurable and manageable—to uncertainty, where unpredictability prevails, deterring capital providers.

Purpose of the Illustration

The spectrum serves as a tool to visually demonstrate how policy decisions affect market stability and capital flow. Our goal is to show that as policies drive the market closer to the "uncertainty" end of the spectrum, capital becomes more scarce, leading to an unstable market environment.

To represent this shift, we use two complementary graphics: the Risk-Uncertainty Spectrum graphic and the Capital Flight graphic. These visuals help illustrate the continuous impact of policies on capital availability, highlighting the relationship between stable policy environments and capital inflow.

3.1 Visual Representation of the Spectrum

The Risk-Uncertainty Spectrum graphic illustrates the market's journey from stability (risk) to volatility (uncertainty). This horizontal spectrum transitions from green on the left, symbolizing a predictable risk environment, to red on the right, representing a volatile and unpredictable market.

Left End (Risk): In a risk-oriented market, data and policies provide a foundation for measurable, manageable outcomes. Capital flows freely, insurance pricing remains stable, and investors feel confident in the predictability of returns.

Right End (Uncertainty): Here, the environment becomes unpredictable and less measurable. As uncertainty increases, investors are more hesitant to allocate capital, fearing unforeseen changes. Insurance premiums rise, market capacity shrinks, and, in severe cases, providers may withdraw entirely from the market.

The placement of a movable indicator on this spectrum illustrates the market's current position. As policies or external conditions evolve, this indicator shifts, highlighting the direct correlation between predictability and capital availability.

Hypothetical Scenario: Autonomous Vehicles and Liability Insurance

· Risk: Suppose an insurance company insures autonomous vehicles based on several years of test data showing a low accident rate in controlled settings. These vehicles have advanced safety features, and the insurer uses this consistent data to assess risk accurately, offering reasonable premiums for known liabilities.

· Uncertainty: If regulators suddenly propose a law holding manufacturers fully liable for all autonomous vehicle accidents, this policy shift introduces uncertainty. The insurer can no longer rely solely on the vehicle's performance data because the financial impact now depends on an unpredictable regulatory environment that could change again based on unforeseen incidents or public concerns.

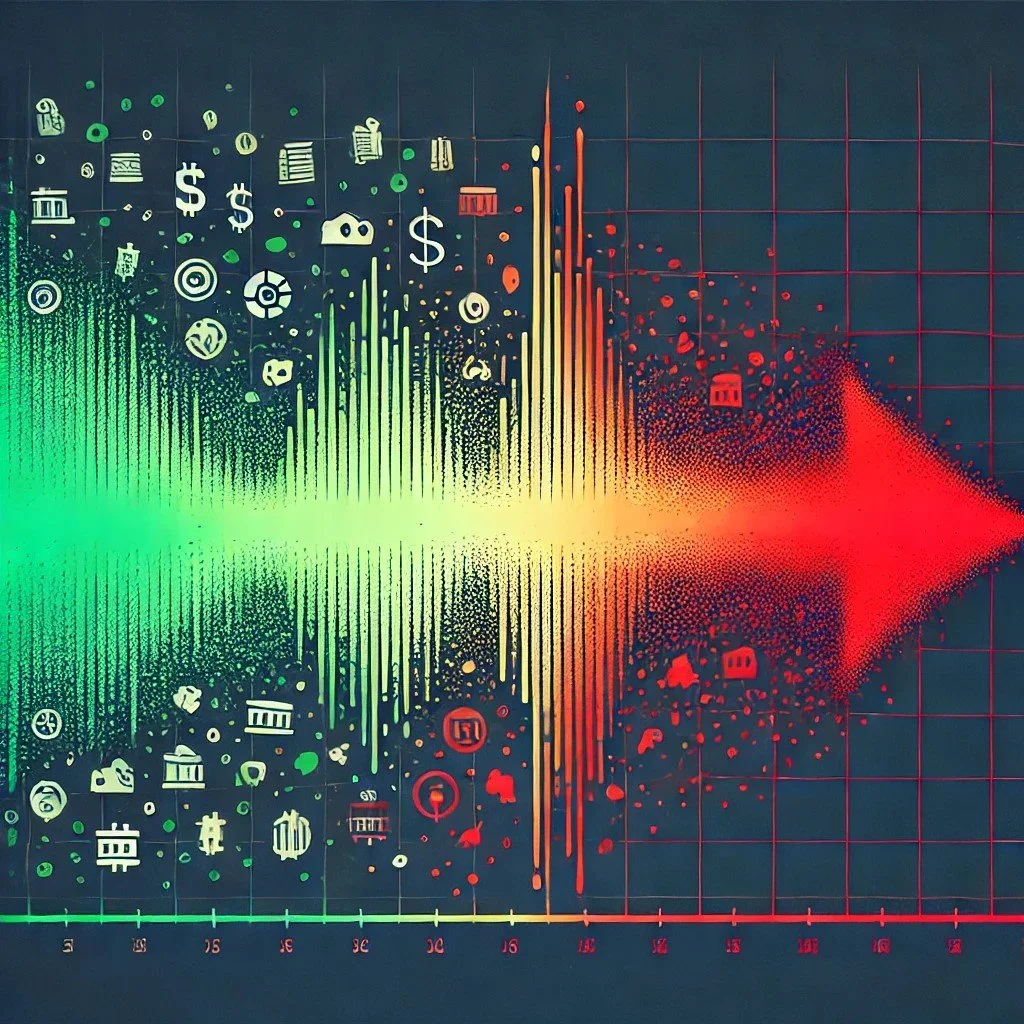

3.2 Capital Response Across the Risk-Uncertainty Spectrum

Capital response to the spectrum's movement underscores the critical role of stability. As the market drifts toward uncertainty, the repercussions for capital availability are immediate and significant.

To visualize this, the Capital Flight graphic provides a metaphor of “evaporation” to capture capital reduction. At the risk end of the spectrum, represented by a full container of water, capital is readily available and flows predictably. Moving across the spectrum toward uncertainty, the water level diminishes and disperses, representing capital flight due to increased volatility. This evaporation effect illustrates how instability actively pushes capital out of catastrophe insurance markets, creating a scarcity that increases premiums and restricts coverage.

3.2.1 Tying Together the Risk-Uncertainty Spectrum and Capital Flight

The Risk-Uncertainty Spectrum and Capital Flight graphics together offer a comprehensive look at how market conditions and policy-driven uncertainty impact capital in catastrophe insurance.

Imagine the Risk-Uncertainty Spectrum as a journey across a landscape from calm, predictable terrain to treacherous, unstable ground. As the market environment shifts along this spectrum from risk to uncertainty, capital investment falters and eventually “evaporates” entirely, leaving an underfunded market. This is not merely a passive transformation; as unpredictability intensifies, investors actively avoid or exit these markets, resulting in higher premiums and fewer coverage options.

The visuals of a fading path and evaporating water in these graphics provide a compelling depiction of the delicate balance insurers and regulators must maintain to foster a sustainable market environment. The continuous spectrum shows that even incremental policy changes can have significant, compounding effects on capital availability, underscoring the need for careful, principle-based policy approaches.

3.3 Factors Influencing Spectrum Position

The position of the indicator on the risk-uncertainty spectrum is not static; it can shift based on various factors that influence the predictability and measurability of outcomes in the catastrophe insurance market. Understanding these factors is crucial for policymakers and market participants to anticipate and manage potential shifts along the spectrum. Let's explore each factor in detail:

1. Data Availability and Quality

The availability and quality of data play a pivotal role in determining where a market falls on the risk-uncertainty spectrum. More comprehensive and reliable data on catastrophe occurrences and their impacts tends to move the indicator leftward towards risk.

· Historical Data: Longer historical records of catastrophic events provide a stronger foundation for risk assessment. For instance, regions with centuries of earthquake data can more accurately model seismic risk compared to areas with limited historical records.

· Data Granularity: The level of detail in available data affects risk assessment accuracy. Highly granular data, such as property-level information on building materials and construction methods, allows for more precise risk pricing.

· Data Consistency: Standardized data collection and reporting methods across different regions and over time enhance the reliability of risk models. Inconsistent or changing data collection methods can introduce uncertainty.

· Real-time Data: The increasing availability of real-time data from sensors, satellites, and other sources can significantly improve risk assessment and early warning systems, potentially shifting the market towards the risk end of the spectrum.

2. Regulatory Stability

The stability and predictability of the regulatory environment have a substantial impact on where the market falls on the spectrum. Consistent, well-defined regulations help maintain a leftward position towards risk.

· Regulatory Clarity: Clear, unambiguous regulations reduce uncertainty for market participants. When insurers and capital providers can easily understand and interpret regulations, they can more confidently assess their risk exposure.

· Regulatory Consistency: Frequent or unpredictable changes in regulations can shift the market towards uncertainty. Conversely, a stable regulatory environment with gradual, well-telegraphed changes helps maintain market stability.

· International Harmonization: In a global reinsurance market, consistency in regulations across jurisdictions can reduce uncertainty. Significant regulatory divergences between countries can complicate risk assessment for international insurers and reinsurers.

· Regulatory Capacity: The ability of regulatory bodies to effectively oversee and enforce regulations affects market stability. Under-resourced or ineffective regulators can inadvertently introduce uncertainty into the market.

3. Policy Interventions

Government policy interventions, while often well-intentioned, can significantly impact the market's position on the risk-uncertainty spectrum. Sudden or poorly conceived policy changes can shift the indicator rightward towards uncertainty.

· Price Controls: Policies that artificially constrain pricing, such as premium caps or mandatory coverage requirements, can distort risk assessment and push the market towards uncertainty.

· Government Backstops: The introduction or modification of government-backed insurance or reinsurance programs can significantly alter market dynamics. While these programs can provide stability in some cases, changes to their structure or funding can introduce uncertainty.

· Tax Policies: Changes in tax treatment of insurance reserves or catastrophe funds can impact insurers' ability to manage risk, potentially shifting the market along the spectrum.

· Building Codes and Land Use Policies: Government decisions on building standards and land use in high-risk areas directly affect the underlying risk landscape. Strengthening these standards generally moves the market towards risk, while relaxing them can increase uncertainty.

4. Market Maturity

The level of development and sophistication of an insurance market influences its position on the spectrum. Well-established markets with a long history tend to have more stability and are often positioned more towards the risk end.

· Market Experience: Markets that have experienced and adapted to multiple catastrophic events over time tend to develop more robust risk assessment and management practices.

· Competitive Dynamics: Mature markets with multiple insurers and reinsurers competing tend to drive innovation in risk assessment and pricing, potentially reducing uncertainty.

· Product Sophistication: Markets with a wide range of insurance products and risk transfer mechanisms (e.g., catastrophe bonds, parametric insurance) are often better equipped to manage complex risks.

· Consumer Awareness: In mature markets, consumers tend to have a better understanding of insurance products and their own risk exposure, leading to more stable demand and potentially reducing uncertainty.

5. Environmental and Climate Changes

Shifts in environmental conditions and climate patterns can significantly impact the predictability of catastrophic events, potentially moving the market along the spectrum.

· Climate Change Impacts: As climate change alters the frequency and severity of weather-related catastrophes, historical data may become less reliable for future predictions, potentially pushing the market towards uncertainty.

· Emerging Risks: The development of new types of catastrophic risks (e.g., cyber risks, pandemic risks) can introduce new elements of uncertainty into the market.

· Scientific Advancements: Improvements in climate modeling and risk prediction can help quantify previously uncertain risks, potentially moving the market back towards the risk end of the spectrum.

· Adaptation Measures: The implementation of large-scale adaptation measures (e.g., flood defenses, wildfire management strategies) can alter the risk landscape, affecting the market's position on the spectrum.

6. Technological Advancements

Technological progress can significantly influence the ability to assess and manage catastrophe risk, often helping to shift the market towards the risk end of the spectrum.

· Improved Modeling Capabilities: Advances in computational power and modeling techniques allow for more sophisticated risk assessments, potentially reducing uncertainty.

· Big Data Analytics: The ability to process and analyze vast amounts of data can lead to more accurate risk predictions and pricing.

· Remote Sensing Technologies: Satellite imagery, drones, and other remote sensing technologies provide more accurate and up-to-date information on risk factors, improving risk assessment capabilities.

· Blockchain and Smart Contracts: These technologies have the potential to increase transparency and efficiency in insurance transactions, potentially reducing certain types of uncertainty in the market.

Understanding these factors and their interplay is crucial for policymakers and market participants. By recognizing how different elements can shift the market along the risk-uncertainty spectrum, stakeholders can work to implement policies and practices that maintain market stability and ensure the availability of affordable catastrophe insurance. Moreover, this understanding can guide efforts to proactively manage and mitigate factors that may push the market towards uncertainty, thereby fostering a more resilient and effective catastrophe insurance ecosystem.

3.4 Practical Illustration: The Journey from Stability to Volatility

To visualize the risk-uncertainty spectrum, we can consider the catastrophe insurance market as a guided journey, where policy predictability plays a key role in maintaining a stable flow of capital.

Risk (Stable Beginning of the Journey)

The journey begins on a well-mapped highway, representing risk. Here, the road is smooth, the lanes are clearly marked, and GPS guidance allows for accurate and predictable navigation. Travelers (investors and insurers) proceed with confidence, aware that while certain roadblocks may arise, the route is largely manageable. In this segment of the journey, insurers can predict potential losses and price policies accordingly, while capital providers feel assured in their investments due to the market’s stability and predictability.

Transitioning Towards Uncertainty

As policies shift unpredictably, imagine our journey leaving the highway and entering an uncharted trail. The clear path fades, the terrain grows rugged, and hazards arise without warning. This represents the shift toward uncertainty, where each policy disruption—be it sudden rate freezes, claims processing changes, or unanticipated regulatory shifts—introduces new unpredictability, deterring investors and insurers from committing capital due to unknown risks. Travelers hesitate or turn back, unwilling to risk the unpredictable path ahead.

Uncertainty (Volatile End of the Journey)

At the furthest end of the journey lies an unpredictable wilderness. Without a defined path, insurers struggle to gauge accurate pricing, and capital providers retract their investments to seek more stable opportunities. Just as travelers avoid venturing deeper into uncharted territory, investors and insurers withdraw when the policy landscape introduces excessive uncertainty.

This journey metaphor emphasizes the necessity of stable policy frameworks to maintain a smooth path for capital flow. When the regulatory environment is as clear and manageable as a well-paved road, investors can confidently commit to the market, ensuring coverage remains affordable and accessible. Conversely, when policy shifts abruptly, the journey becomes uncertain, diminishing capital availability and destabilizing the market overall.

3.5 Implications for Policymakers

The risk-uncertainty spectrum provides policymakers with a powerful conceptual tool for assessing and managing the potential impact of their decisions on catastrophe insurance markets. By visualizing the market's position on this spectrum, policymakers can better understand the consequences of their actions and craft more effective, balanced regulations. Let's explore the key implications and applications of this framework for policymakers in greater detail:

3.5.1 Policy Assessment and Impact Analysis

The risk-uncertainty spectrum serves as a valuable tool for evaluating proposed policies before implementation:

· Pre-Implementation Analysis: Before enacting new regulations, policymakers should conduct a thorough analysis of how the proposed changes might shift the indicator on the spectrum. This involves:

o Consulting with industry experts, actuaries, and economists to model potential outcomes

o Examining case studies from other jurisdictions that have implemented similar policies

o Conducting stakeholder consultations to understand potential market reactions

· Quantitative Metrics: Develop and track quantitative metrics that correlate with the market's position on the spectrum, such as:

o Capital inflow/outflow in the insurance sector

o Changes in policy pricing and availability

o Market concentration indices

o Reinsurance costs and availability

· Scenario Planning: Use the spectrum as a basis for scenario planning exercises, modeling how different policy options might move the market under various conditions.

· Cumulative Impact Assessment: Consider not just the impact of individual policies, but their cumulative effect when combined with existing regulations and market conditions.

3.5.2 Gradual Implementation Strategies

Recognizing that sudden shifts towards uncertainty can destabilize markets, policymakers should prioritize gradual, predictable policy implementation:

· Phased Rollouts: For policies likely to significantly impact the market, consider a phased implementation approach:

o Start with pilot programs in limited geographic areas or market segments

o Establish clear milestones and evaluation criteria for each phase

o Allow for adjustments based on observed outcomes before full implementation

· Transition Periods: Provide adequate transition periods for market participants to adapt to new regulations:

o Set realistic timelines that account for the complexity of changes required

o Consider the different capacities of large vs. small market players to implement changes

· Adaptive Regulation: Design policies with built-in flexibility to adjust based on market responses:

o Include provisions for periodic reviews and adjustments

o Establish clear triggers or thresholds for when adjustments may be necessary

3.5.3 Balancing Act: Consumer Protection and Market Stability

One of the most critical challenges for policymakers is maintaining a balance between protecting consumers and ensuring market stability:

· Risk-Based Approach: Adopt a risk-based approach to regulation that focuses on addressing specific, identified risks rather than implementing broad, one-size-fits-all policies.

· Consumer Education: Invest in consumer education programs to help policyholders understand their risks and make informed decisions:

o Develop clear, accessible materials explaining insurance products and risk factors

o Partner with community organizations and insurance agents to disseminate information

· Market Monitoring: Establish robust market monitoring systems to detect early signs of instability or consumer harm:

o Regular data collection and analysis on market trends

o Establish channels for consumer feedback and complaints

· Regulatory Impact Assessments: Conduct regular assessments of how existing regulations are affecting both consumer protection and market stability:

o Identify and address any unintended consequences

o Look for opportunities to streamline or simplify regulations without compromising protection

3.5.4 Communication and Transparency

Clear communication about policy decisions and their rationale is crucial for maintaining market confidence:

· Stakeholder Engagement: Develop robust processes for engaging with all stakeholders, including insurers, consumers, and intermediaries:

o Regular roundtable discussions or forums

o Public consultation periods for proposed regulations

o Transparent reporting on how stakeholder input is incorporated into decision-making

· Clear Policy Roadmaps: Provide clear, long-term policy roadmaps to give market participants visibility into future regulatory direction:

o Outline long-term goals and the steps to achieve them

o Regularly update these roadmaps based on changing conditions and new information

· Explaining the Spectrum: Use the risk-uncertainty spectrum as a communication tool to explain policy decisions to stakeholders:

o Visualize how proposed changes might affect market stability

o Demonstrate the trade-offs involved in different policy options

3.5.5 Fostering Innovation and Market-Based Solutions

Policymakers can use the spectrum to guide efforts in encouraging innovation that helps manage catastrophe risk:

· Regulatory Sandboxes: Establish regulatory sandboxes to allow controlled testing of innovative insurance products or business models:

o Set clear parameters for experimentation while maintaining consumer protections

o Use insights from these experiments to inform broader policy decisions

· Incentivizing Risk Reduction: Develop policies that incentivize risk reduction measures:

o Tax incentives for property improvements that reduce catastrophe risk

o Partnerships with insurers to offer premium discounts for risk mitigation efforts

· Supporting Alternative Risk Transfer: Encourage the development and use of alternative risk transfer mechanisms:

o Provide regulatory clarity on the treatment of instruments like catastrophe bonds

o Consider public-private partnerships to develop new risk transfer solutions

3.5.6 International Coordination

Given the global nature of reinsurance markets, policymakers should consider international implications of their decisions:

· Regulatory Harmonization: Work towards greater harmonization of regulations across jurisdictions:

o Participate in international forums and standard-setting bodies

o Consider how local regulations interact with international markets

· Cross-Border Information Sharing: Establish mechanisms for sharing information and best practices with regulators in other jurisdictions:

o Collaborative research on emerging risks and regulatory approaches

o Joint scenario planning exercises

3.5.7 Continuous Learning and Adaptation

The dynamic nature of catastrophe risks requires a commitment to continuous learning and adaptation:

· Regular Policy Reviews: Establish a schedule for regular, comprehensive reviews of the regulatory framework:

o Assess the cumulative impact of regulations on market stability

o Identify opportunities for simplification or modernization

· Investing in Research: Support ongoing research into catastrophe risk, climate change impacts, and effective regulatory approaches:

o Fund academic studies and collaborate with research institutions

o Use research findings to inform policy adjustments

· Skill Development: Invest in developing the skills and knowledge of regulatory staff:

o Training programs on emerging risks and regulatory techniques

o Exchanges or secondments with industry to build practical understanding

By embracing these implications and actively using the risk-uncertainty spectrum as a guiding framework, policymakers can craft more effective, balanced regulations for catastrophe insurance markets. This approach can help ensure that policies achieve their consumer protection goals while maintaining the market stability necessary for long-term sustainability and resilience in the face of catastrophic events.

The risk-uncertainty spectrum provides policymakers with a valuable tool for assessing the potential impact of their decisions.

4. Policy Decisions and Unintended Consequences: A Case Study of Hurricane Insurance in Florida

The intricate dance between policy decisions and market dynamics is nowhere more evident than in Florida's hurricane insurance market. As a region with high exposure to catastrophic events, Florida serves as a critical case study for understanding how policy interventions can inadvertently shift the market along the risk-uncertainty spectrum, leading to unintended consequences that often undermine the very goals policymakers aim to achieve.

4.1 Policy Goals vs. Market Realities

Policy decisions in catastrophe insurance markets often aim to achieve one or more of the following goals:

Stabilize markets

Protect consumers

Manage costs

Ensure widespread coverage availability

However, without thorough market analysis and consideration of long-term consequences, these well-intentioned policies can create unanticipated instability. The disconnect between policy goals and market realities often stems from a misunderstanding of the delicate balance between risk and uncertainty in insurance markets.

4.1.1 Rate Freezes and Price Controls

· Intended Goal: Keep premiums affordable for consumers.

· Policy Mechanism: Legislatively imposed caps on premium increases or freezes on rates, particularly for state-run insurers.

· Market Reality: These policies can limit insurers' flexibility to adjust prices based on evolving risk assessments. When insurers are unable to cover their costs or maintain adequate reserves, they may:

o Reduce coverage options, leaving consumers with less comprehensive protection

o Withdraw from high-risk areas, creating coverage deserts in vulnerable regions

o Exit the market entirely, reducing competition and potentially leading to even higher prices in the long run

Example from Florida: In 2007, following the intense hurricane seasons of 2004-2005, Florida enacted a law that froze rates for the state-run Citizens Property Insurance Corporation and required private insurers to essentially match these rates[5]. While this provided short-term relief to homeowners, it set the stage for long-term market instability.

Unintended Consequences:

Private insurers, unable to charge actuarially sound rates, began to withdraw from the Florida market or reduce their exposure.

Citizens Property Insurance Corporation grew dramatically, concentrating risk in a state-run entity and increasing potential taxpayer liability.

The suppressed rates failed to signal the true cost of living in high-risk areas, potentially encouraging further development in vulnerable coastal regions.

4.1.2 Legislative Interventions in Claims Processes

· Intended Goal: Ensure fair and timely claims processing for policyholders.

· Policy Mechanism: Laws that modify claims handling procedures, extend statutes of limitations for filing claims, or change the burden of proof in claims disputes.

· Market Reality: Sudden changes to claims processes, especially when applied retroactively, create an unpredictable claims environment. This leads to:

o Uncertainty in loss projections, making it difficult for insurers to price policies accurately

o Increased litigation, driving up costs for insurers and, ultimately, policyholders

o Hesitancy from capital providers who see these markets as unreliable investments

Example from Florida: In 2019, Florida passed a law allowing homeowners to file claims up to three years after a hurricane, extending the previous deadline of two years[6]. While intended to protect homeowners, this change introduced significant uncertainty for insurers.

Unintended Consequences:

Insurers faced increased difficulty in closing their books on past events, leading to ongoing financial uncertainty.

The extended claim period potentially incentivized fraudulent claims, as damage from other causes could be attributed to past storms.

Reinsurers, facing increased uncertainty, raised rates or reduced capacity in Florida, driving up costs for primary insurers and, ultimately, consumers.

4.1.3 Mandated Coverage Expansions

· Intended Goal: Ensure comprehensive protection for policyholders.

· Policy Mechanism: Requiring insurers to cover additional perils or expand coverage without the ability to adequately price for the increased risk.

· Market Reality: When insurers are required to cover additional perils or expand coverage without the ability to adequately price for the increased risk, it can lead to:

o Underpricing of policies, threatening insurer solvency

o Overpricing in other areas to compensate, making coverage less affordable

o Reduced market participation as insurers seek more predictable markets

Example from Florida: In 2019, Florida required insurers to provide coverage for windstorm and contents without a separate deductible in certain cases, aiming to simplify policies for consumers[7].

Unintended Consequences:

Some insurers responded by raising overall premiums to account for the increased risk exposure.

Others reduced their writing of new policies in high-risk coastal areas, limiting consumer choice.

The one-size-fits-all approach reduced policy customization options for consumers who might have preferred lower premiums with higher deductibles.

4.2 Case Study: Florida's Hurricane Insurance Regulation

Florida's experience with hurricane insurance regulation provides a compelling illustration of how policy decisions can shift the market along the risk-uncertainty spectrum, leading to unintended consequences that often undermine the very goals policymakers aim to achieve.

4.2.1 Historical Context

Florida's vulnerability to hurricanes has long posed challenges for its insurance market. However, the crisis that reshaped the state's approach to insurance regulation was precipitated by an unprecedented series of events:

2004-2005 Hurricane Seasons: Florida was struck by eight hurricanes in two years, including the devastating Hurricane Wilma in 2005. These storms resulted in over $30 billion in insured losses[8].

Market Exodus: In the aftermath of these hurricanes, many national insurers began to reduce their exposure in Florida or exit the market entirely. Notable departures included State Farm, which announced plans to withdraw from the Florida property insurance market in 2009[9].

Rising Premiums: As insurers reassessed their risk exposure, many sought significant premium increases, some as high as 200-300%[10].

Political Pressure: The combination of reduced availability and skyrocketing premiums created intense political pressure for government intervention.

This confluence of events set the stage for a series of regulatory interventions that would dramatically reshape Florida's insurance landscape.

4.2.2 Key Policy Interventions

In response to the crisis, Florida enacted a series of regulatory measures aimed at stabilizing the market and protecting consumers. However, these interventions, while well-intentioned, often had complex and sometimes counterproductive effects on the market:

Rate Freezes (2007)

Policy: The Florida Legislature passed a law freezing rates for the state-run Citizens Property Insurance Corporation and requiring private insurers to essentially match these rates[11].

Intention: To provide immediate relief to homeowners facing sharp premium increases.

Effect: This policy shifted the market towards uncertainty by disconnecting premiums from actuarial risk.

Expansion of the Florida Hurricane Catastrophe Fund (2007)

Policy: The state significantly increased the capacity of this fund, which provides reinsurance to insurers at below-market rates[12].

Intention: To reduce reinsurance costs for insurers, allowing them to offer lower premiums to consumers.

Effect: While providing short-term relief, this policy increased the state's financial exposure to a major hurricane event.

Restrictions on Non-Renewals (2007)

Policy: Insurers were prohibited from non-renewing or cancelling a large number of policies in the wake of the hurricanes[13].

Intention: To prevent a sudden loss of coverage for homeowners.

Effect: This policy limited insurers' ability to manage their risk exposure, potentially discouraging new entrants to the market.

Citizens "Glide Path" (2009)

Policy: Introduction of a "glide path" allowing Citizens to raise rates by up to 10% per year[14].

Intention: To gradually move Citizens' rates towards actuarially sound levels without shocking the market.

Effect: While more measured than a rate freeze, this policy still constrained insurers' ability to adjust to changing risk assessments.

Claims Filing Extension (2019)

Policy: Extension of the deadline for filing hurricane claims from two years to three years after the storm[15].

Intention: To provide homeowners more time to discover and report damage.

Effect: This policy introduced additional uncertainty into the claims process, complicating insurers' ability to close their books on past events.

4.2.3 Initial Impact

In the short term, these policies appeared to achieve their goals:

Premium Stabilization: Rates stabilized or decreased for many homeowners, providing immediate financial relief.

Market Retention: The restrictions on non-renewals prevented a sudden exodus of insurers from the market.

Coverage Availability: The expansion of Citizens and the Cat Fund ensured that coverage remained available, even as private insurers reduced their exposure.

Political Win: Policymakers were able to demonstrate responsive action to their constituents' concerns about rising insurance costs.

These initial outcomes were largely viewed as positive by the public and many policymakers, seeming to justify the interventionist approach. However, as we'll explore in the next section, the long-term consequences of these policies would prove far more complex and often counterproductive.

4.2.4 Long-Term Consequences

As time passed, the unintended consequences of these policies became increasingly apparent, shifting the market towards the uncertainty end of our spectrum:

1. Capital Flight

· Manifestation: Unable to adjust premiums to cover rising risks, many private insurers faced unsustainable losses. This prompted capital providers to withdraw from the Florida market, viewing it as an unpredictable and potentially unprofitable investment.

· Data Point: Between 2017 and 2022, five property insurers became insolvent, and at least a dozen more voluntarily left the Florida market[16].

· Spectrum Shift: This outcome pushed the market significantly towards uncertainty, as the reduced number of insurers and the exit of established players increased volatility and reduced predictability.

2. Market Concentration

· Manifestation: As private insurers retreated, the state-run Citizens Property Insurance Corporation grew to become one of the largest property insurers in Florida, concentrating risk in a single, state-backed entity.

· Data Point: Citizens' policy count grew from about 420,000 in 2019 to over 1.3 million in 2023[17].

· Spectrum Shift: This concentration of risk in a single entity increased the systemic risk in the market, moving it further towards uncertainty.

3. Reduced Competition

· Manifestation: With fewer private insurers in the market, competition decreased, ultimately leading to fewer choices and, paradoxically, higher premiums for consumers in the long run.

· Data Point: The average Florida homeowners insurance premium increased by 33% between 2016 and 2021, compared to a national average increase of 11%[18].

· Spectrum Shift: The reduced competition and higher premiums signaled a market moving away from efficiency and predictability, characteristics associated with the "risk" end of our spectrum.

4. Increased Vulnerability

· Manifestation: The expansion of the Florida Hurricane Catastrophe Fund, while providing short-term relief, increased the state's financial exposure to a major hurricane event, potentially putting taxpayers at risk.

· Data Point: As of 2022, the Cat Fund had a claims-paying capacity of $17 billion, but a major hurricane could potentially exhaust this capacity[19].

· Spectrum Shift: This increased state exposure introduced a new element of uncertainty into the market, as the sustainability of this backstop in the face of a major catastrophe remained questionable.

5. Litigation Explosion

· Manifestation: Changes to claims processes and deadlines led to an explosion in litigation, driving up costs for insurers and ultimately policyholders.

· Data Point: In 2019, Florida accounted for 76% of all homeowners insurance litigation in the U.S., despite representing only 8% of all homeowners claims[20].

· Spectrum Shift: The unpredictability and cost of litigation pushed the market further towards uncertainty, making it difficult for insurers to accurately price policies and manage risk.

· When litigation in catastrophe insurance markets surge, it introduces substantial costs and increased unpredictability, creating further deterrents for insurance and reinsurance providers. Prior to 2022, despite representing only 8% of all U.S. homeowners insurance claims, Florida accounted for a striking 76% of the nation’s homeowners insurance litigation. This litigious environment amplified uncertainty, making it difficult for insurers to set stable rates and manage risk effectively.

To address these challenges, Senate Bill 2-A was enacted in late 2022, introducing significant reforms aimed at reducing litigation and stabilizing the property insurance market. Key provisions included:

o Reducing frivolous lawsuits: Measures to curb excessive litigation against insurers, helping prevent premium inflation driven by legal costs.

o Mandating faster claim processing: Requirements for insurers to expedite claims, ensuring quicker resolution for policyholders.

o Granting home-hardening incentives: Providing funds to help homeowners reinforce properties against hurricanes and other natural disasters.

o Increasing insurance affordability and availability: Aiming to attract insurers back to the market and offer more affordable options for Floridians.

These reforms represent a significant step toward mitigating the impacts of litigation and market uncertainty. Although the full effects of Senate Bill 2-A may take time to materialize, this legislative action illustrates how structured policy changes can address market instability and improve consumer outcomes.

4.3 Illustration of Risk-Adjusted Spectrum in Policy Context

To better understand how these policy decisions shifted Florida's insurance market along the risk-uncertainty spectrum, let's visualize the progression:

Initial State (Pre-2004):

Risk [--|----------------------------------------] Uncertainty

^

Market State

The market was relatively stable, with the indicator positioned closer to the risk end. Capital providers were confident in their ability to assess and price hurricane risk based on historical data and models.

2. Post-Hurricane Crisis (2005-2006):

Risk [---------------------------------------------|---] Uncertainty

^

Market State

The unprecedented hurricane seasons pushed the market towards uncertainty, as existing models proved inadequate for the scale of losses experienced.

Immediate Post-Regulation Period (2007-2008):

Risk [----------------------|-------------------------] Uncertainty

^

Market State

The regulatory interventions initially appeared to stabilize the market, pulling the indicator slightly back towards risk. However, the artificial constraints on pricing and risk assessment began to introduce new forms of uncertainty.

4. Long-Term Impact (2010 onwards):

As the long-term consequences of the regulatory interventions became apparent, the market shifted significantly towards uncertainty. The inability to accurately price risk, combined with the concentration of risk in state-backed entities, created an environment that deterred private capital investment.

This progression illustrates how well-intentioned policy decisions, aimed at protecting consumers and stabilizing the market in the short term, can have the unintended consequence of pushing the market towards greater uncertainty in the long run.

4.4 Broader Comparisons and Lessons Learned

The Florida case study provides valuable insights that can be applied to other regulated industries and catastrophe insurance markets worldwide. Similar dynamics are seen in various sectors where regulatory interventions aimed at consumer protection or market stabilization can lead to unintended consequences.

4.4.1 Healthcare Markets

In many countries, healthcare markets face similar challenges when policymakers attempt to control costs or expand access through regulatory measures:

1. Price Controls

· Policy Example: Government-imposed caps on insurance premium increases or mandated coverage for pre-existing conditions without adequate risk adjustment.

· Intended Goal: Make healthcare more affordable and accessible.

· Unintended Consequences:

o Insurers may exit markets where they cannot operate profitably.

o Reduced investment in innovative treatments or technologies.

o Potential for reduced quality of care as providers struggle to maintain profitability under price constraints.

2. Coverage Mandates

· Policy Example: Requirements for insurers to cover specific conditions or treatments without the ability to adjust premiums accordingly.

· Intended Goal: Ensure comprehensive coverage for all consumers.

· Unintended Consequences:

o Increased premiums for all policyholders to cover the mandated benefits.

o Potential for adverse selection, where only high-risk individuals purchase coverage.

o Market distortions as insurers try to avoid high-risk populations.

4.4.2 Energy Markets

Energy sectors, particularly in regions transitioning to renewable sources, often face regulatory challenges that mirror those in catastrophe insurance:

1. Subsidies and Price Guarantees

· Policy Example: Feed-in tariffs for renewable energy or production tax credits for certain energy sources.

· Intended Goal: Encourage investment in new technologies and accelerate the transition to clean energy.

· Unintended Consequences:

o Distortion of market signals, potentially leading to overinvestment in subsidized technologies.

o Difficulty in phasing out subsidies once industries become dependent on them.

o Potential for increased energy costs for consumers as subsidies are factored into overall energy pricing.

2. Rapid Policy Changes

· Policy Example: Sudden shifts in energy policy, such as abrupt changes to renewable energy incentives or nuclear power regulations.

· Intended Goal: Respond to new information or changing public sentiment about energy sources.

· Unintended Consequences:

o Uncertainty that deters long-term investment in energy infrastructure.

o Stranded assets as investments made under previous policy regimes become uneconomical.

o Potential for supply

4.4.3 Lessons for Policymakers

Drawing from the Florida case study and the broader comparisons in healthcare and energy markets, several key lessons emerge for policymakers. These insights can guide the development of more effective and balanced regulatory approaches in catastrophe insurance and other complex markets:

1. Adopt a Long-Term Perspective

Lesson: Policies should be evaluated not just for their immediate impact but for their long-term consequences on market stability and capital availability.

Application:

· Conduct comprehensive impact assessments that model policy effects over 5, 10, and 20-year horizons.

· Incorporate scenario planning to anticipate potential market responses and adapt policies accordingly.

· Establish regular review periods to assess the ongoing effectiveness and relevance of policies.

Example: Florida's rate freeze policy, while providing immediate relief to consumers, led to long-term market instability. A more balanced approach might have involved gradual rate adjustments coupled with targeted subsidies for vulnerable populations.

2. Respect Market Mechanisms

Lesson: Wherever possible, allow market mechanisms to function in pricing risk and allocating capital. Interventions should be carefully considered and implemented only when absolutely necessary.

Application:

· Focus on creating a regulatory framework that enhances market transparency and competition rather than directly controlling prices.

· When intervention is necessary, use market-based tools (e.g., incentives, tradable permits) rather than command-and-control regulations.

· Encourage innovation in risk transfer mechanisms, such as catastrophe bonds or parametric insurance products.

Example: Instead of freezing rates, Florida could have focused on improving risk modeling and data transparency, allowing insurers to price risks more accurately while fostering competition to keep premiums in check.

3. Implement Gradual Changes

Lesson: When regulatory changes are needed, implement them gradually to allow markets time to adjust and to minimize uncertainty.

Application:

· Use phased implementation schedules for significant policy changes.

· Establish clear, predictable timelines for regulatory adjustments.

· Incorporate feedback loops to allow for course corrections during implementation.

Example: The "glide path" approach for Citizens Insurance rate increases was a step in the right direction, allowing for more gradual market adjustment compared to the earlier rate freeze.

4. Engage Stakeholders Comprehensively

Lesson: Engage with industry experts, insurers, consumers, and economists to craft policies that maintain market stability without stifling competition or innovation.

Application:

· Establish formal consultation processes that include a diverse range of stakeholders.

· Create advisory panels that bring together experts from various fields to inform policy development.

· Conduct public hearings and comment periods to gather broad input on proposed regulations.

Example: Florida's policy-making process could have benefited from more extensive engagement with reinsurers and capital markets to understand how proposed regulations might affect capital flows into the state's insurance market.

5. Build Flexibility and Adaptability into Regulatory Frameworks

Lesson: Build flexibility into regulatory frameworks to allow for adjustments based on changing market conditions or new data.

Application:

· Incorporate sunset clauses or automatic review triggers in legislation.

· Establish regulatory sandboxes to test innovative approaches before full implementation.

· Develop adaptive management frameworks that allow for policy adjustments based on predefined indicators.

Example: Florida's claims filing extension could have included provisions for reassessment based on its impact on litigation rates and insurer solvency.

6. Prioritize Transparency and Clear Communication

Lesson: Clearly communicate the rationale behind policy decisions and provide predictable timelines for implementation to reduce uncertainty for market participants.

Application:

· Develop comprehensive communication strategies for all major policy initiatives.

· Publish regular reports on the state of the insurance market and the impact of regulations.

· Create educational programs to help consumers understand insurance products and regulatory changes.

Example: Florida could have better communicated the long-term strategy behind its regulatory interventions, helping stakeholders understand and prepare for future market conditions.

7. Balance Consumer Protection with Market Sustainability

Lesson: Recognize that excessive focus on short-term consumer protection can undermine long-term market stability and ultimately harm consumers.

Application:

· Develop policies that protect vulnerable consumers without distorting the entire market.

· Focus on improving financial literacy and risk awareness among consumers.

· Consider the use of targeted subsidies or vouchers instead of broad market interventions.

Example: Instead of broad rate suppression, Florida could have developed targeted assistance programs for low-income homeowners in high-risk areas.

8. Invest in Risk Mitigation and Resilience

Lesson: Recognize that reducing underlying risks can be more effective than manipulating insurance markets.

Application:

· Invest in infrastructure improvements that reduce catastrophe risk.

· Develop and enforce stricter building codes in high-risk areas.

· Create incentives for individual and community-level risk reduction efforts.

Example: Florida's focus on insurance regulation could have been complemented by more aggressive investment in hurricane-resistant infrastructure and stricter enforcement of building codes in coastal areas.

9. Coordinate Across Jurisdictions

Lesson: In interconnected markets like insurance, coordination across state and national boundaries is crucial for effective regulation.

Application:

· Participate in inter-state and international regulatory forums.

· Strive for consistency in regulatory approaches across jurisdictions.

· Develop mechanisms for information sharing and collective action in response to market challenges.

Example: Florida could have coordinated more closely with other hurricane-prone states to develop consistent approaches to catastrophe insurance regulation, potentially creating a larger, more stable risk pool.

10. Leverage Data and Technology

Lesson: Embrace technological advancements and data analytics to improve risk assessment and policy design.

Application:

· Invest in advanced catastrophe modeling capabilities.

· Utilize big data analytics to gain deeper insights into market dynamics.

· Explore the use of blockchain and smart contracts to increase market efficiency and transparency.

Example: Florida could have invested more heavily in state-of-the-art hurricane modeling and data analytics capabilities to inform both insurers and regulators, potentially reducing uncertainty in the market.

By applying these lessons, policymakers can work towards creating a regulatory environment that balances consumer protection with market stability, keeping the indicator on our risk-uncertainty spectrum as close to the "risk" end as possible. This approach can lead to more resilient insurance markets that are better equipped to handle catastrophic events while providing affordable and reliable coverage to consumers.

5. The Economic Consequence of Increasing Uncertainty

As markets move from risk to uncertainty on our spectrum, they face several detrimental effects that can have far-reaching consequences for both the insurance industry and the broader economy. Understanding these effects is crucial for policymakers and stakeholders to grasp the full impact of decisions that increase market uncertainty.

5.1 Capital Flight Dynamics

One of the most immediate and significant consequences of increasing uncertainty is capital flight. This phenomenon occurs when investors and capital providers, faced with an unpredictable market environment, choose to reallocate their resources to more stable and predictable sectors.

5.1.1 Mechanisms of Capital Flight

1. Risk-Adjusted Return Calculations

As uncertainty increases, investors struggle to accurately calculate risk-adjusted returns. This leads to several consequences:

· Higher Risk Premiums: Investors demand higher returns to compensate for the perceived increase in risk. This can be quantified through measures like the Sharpe ratio or the information ratio, which may decline as uncertainty rises.

· Example: In Florida, following the 2004-2005 hurricane seasons and subsequent regulatory interventions, reinsurance costs for Florida insurers increased by an average of 76% between 2006 and 2009[21].

· Reduced Willingness to Commit Long-term Capital: Investors become hesitant to lock up capital in long-term investments when the future regulatory and risk landscape is unclear.

· Example: The number of private insurers writing homeowners policies in Florida decreased from 119 in 2006 to 89 in 2010, indicating a reluctance to commit to the market long-term[22].

· Preference for More Liquid Investments: Capital providers shift towards investments that allow for quick exit strategies, potentially moving away from traditional reinsurance arrangements towards more liquid alternatives like catastrophe bonds.

· Example: The global catastrophe bond market grew from $22.5 billion in 2007 to over $50 billion in 2021, partly driven by investors seeking more liquid exposure to insurance risks[23].

2. Regulatory Arbitrage

Capital may flow to jurisdictions with more predictable regulatory environments, creating a "race to the bottom" where regions compete for investment by offering the most favorable (and potentially less stringent) regulatory conditions.

· Cross-border Capital Flows: Insurers and reinsurers may shift their capital allocation to regions with more stable regulatory environments.

· Example: Following Florida's regulatory interventions, some major insurers like State Farm significantly reduced their exposure in Florida while expanding in other states[24].

· Offshore Reinsurance: Increased use of offshore reinsurance arrangements to bypass stringent local regulations.

· Example: The use of offshore reinsurance by Florida domestic insurers increased by 30% between 2006 and 2011[25].

3. Sector Rotation

Within the insurance industry, capital may shift from catastrophe-prone lines to more predictable lines of business, leaving catastrophe insurance markets underserved.

· Shift to Less Volatile Lines: Insurers may reduce their exposure to property insurance in favor of other lines like auto or life insurance.

· Example: In Florida, while property insurance premiums grew by only 5% between 2006 and 2010, auto insurance premiums grew by 15% in the same period, indicating a shift in focus[26].

· Geographic Diversification: Insurers may spread their risk across different regions to reduce exposure to any single regulatory regime.

· Example: Following the Florida crisis, national insurers like Allstate and Nationwide significantly reduced their market share in Florida while expanding in other states[27].

5.1.2 Impact on Market Capacity

The flight of capital directly impacts the capacity of the insurance market to provide coverage:

1. Reduced Underwriting Capacity

With less capital available, insurers are forced to reduce the number and size of policies they can underwrite.

· Policy Limits: Insurers may lower coverage limits or introduce stricter sub-limits for certain perils.

· Example: In Florida, the average policy limit for wind coverage decreased by 10% between 2006 and 2010[28].

· Non-renewals: Insurers may choose not to renew policies in high-risk areas.

· Example: In 2009, State Farm announced plans to non-renew 125,000 policies in Florida[29].

2. Market Consolidation

Smaller insurers, unable to weather periods of uncertainty, may be forced out of the market or acquired by larger entities, reducing competition.

· Insolvencies: Increased uncertainty can lead to more insurer insolvencies, particularly among smaller, less diversified companies.

· Example: Between 2017 and 2022, at least seven Florida-based property insurers became insolvent[30].

· Mergers and Acquisitions: Larger insurers may acquire smaller ones to gain market share or diversify risk.

· Example: The number of Florida domestic property insurers decreased from 70 in 2014 to 52 in 2021, partly due to consolidation[31].

3. Increased Reliance on Government Backstops

As private capital retreats, there's often increased pressure on government-backed insurance programs to fill the gap, potentially increasing taxpayer risk.

· Growth of State-run Insurers: Government-backed insurers of last resort may see rapid growth.

· Example: Florida's Citizens Property Insurance Corporation saw its policy count grow from about 420,000 in 2019 to over 1.3 million in 2023[32].

· Expansion of Government Reinsurance: State or federal reinsurance programs may need to expand to support the market.

· Example: The Florida Hurricane Catastrophe Fund's mandatory coverage increased from $15 billion in 2006 to $17 billion in 2021[33].

5.2 Direct Impact on Policyholders

The consequences of capital flight and increased uncertainty are ultimately borne by policyholders in several ways:

5.2.1 Premium Increases

As capital becomes scarce and more expensive, insurers face higher costs, which are often passed on to consumers through increased premiums.

1. Affordability Issues:

o Higher premiums can make insurance unaffordable for many homeowners, particularly in high-risk areas.

o Example: The average Florida homeowners insurance premium increased by 33% between 2016 and 2021, compared to a national average increase of 11%[34].

2. Potential for Coverage Gaps:

o As some consumers are priced out of the market, they may choose to go uninsured or underinsured.

o Example: A 2020 survey found that 13% of Florida homeowners had no property insurance, citing cost as the primary reason[35].

3. Increased Financial Strain:

o Higher insurance costs can put additional financial pressure on households and businesses.

o Example: In 2022, insurance costs were cited as a major factor in Florida's affordability crisis, with some homeowners reporting insurance costs higher than their mortgages[36].

5.2.2 Reduced Coverage Options

With fewer insurers in the market and reduced capacity, policyholders may face:

1. Limited Choice in Insurance Providers:

o Fewer insurers mean less competition and fewer options for consumers.

o Example: The number of private insurers writing homeowners policies in Florida decreased from 119 in 2006 to 89 in 2010[37].

2. Restrictive Policy Terms and Conditions:

o Insurers may introduce more exclusions or higher deductibles to manage their risk exposure.

o Example: Many Florida insurers began requiring separate, higher deductibles for hurricane damage, sometimes as high as 5% of the insured value[38].

3. Difficulty Obtaining Coverage in Certain Areas:

o High-risk areas may see a significant reduction in available coverage options.

o Example: In some coastal counties of Florida, over 50% of homeowners were forced into the state-run insurer of last resort due to lack of private market options[39].

5.2.3 Increased Vulnerability

The reduced capacity for catastrophe coverage leaves disaster-prone regions more vulnerable:

1. Underinsurance Becomes More Common:

o Faced with higher premiums, many policyholders may opt for lower coverage limits.

o Example: A 2021 study found that 64% of homes in Florida were underinsured by an average of 18%[40].

2. Slower Economic Recovery from Disasters:

o Inadequate insurance coverage can slow down rebuilding efforts and economic recovery following a catastrophe.

o Example: After Hurricane Michael in 2018, communities with lower insurance penetration showed slower recovery rates, with some areas still struggling three years later[41].

3. Increased Burden on Public Resources:

o As private insurance becomes less available or affordable, there's greater reliance on public assistance following disasters.

o Example: FEMA reported a 20% increase in flood insurance claims from uninsured Florida properties between 2015 and 2020, indicating a growing burden on federal disaster assistance programs[42].

These impacts on policyholders demonstrate how uncertainty in the insurance market can have far-reaching consequences, affecting not just the financial health of individuals and businesses, but also the overall resilience and recovery capacity of disaster-prone communities. The challenge for policymakers is to find ways to maintain market stability and capital availability while ensuring that insurance remains accessible and affordable for those who need it most.

5.3 Long-Term Market Instability

Persistent uncertainty can lead to a cycle of instability that is difficult to break:

1. Underinvestment in Risk Management: With capital scarce, there may be reduced investment in risk modeling, mitigation strategies, and infrastructure improvements that could help manage catastrophe risk more effectively.

2. Loss of Expertise: As insurers exit the market or reduce their catastrophe exposure, there's a potential loss of specialized knowledge and expertise in managing these unique risks.

3. Boom-Bust Cycles: The catastrophe insurance market may become subject to more pronounced boom-bust cycles, with capital flooding in during periods of low catastrophe activity and rapidly exiting following major events or regulatory changes.

4. Erosion of Public Trust: Frequent market disruptions and coverage issues can erode public trust in the insurance industry and regulatory bodies, making future reforms more challenging.

5.4 Analogy: The "Concert Effect"

To illustrate these concepts in a more relatable way, consider the catastrophe insurance market as a concert venue:

· The Venue: Represents the insurance market

· The Musicians: Insurers providing coverage

· The Audience: Capital providers and investors

· The Performance: The ongoing operation of the insurance market

When risk is predictable (the concert is well-organized and the music genre is known), investors are like concertgoers filling up seats, excited for the performance. But as policies introduce uncertainty, it's as if the concert suddenly changes genres or the venue starts shifting unpredictably. Many audience members (investors) leave, uncomfortable with the new, unpredictable environment.

Those who stay demand a premium experience (higher returns) for tolerating the unpredictable atmosphere. Some may move to the back of the venue (reduced commitment) to maintain an easy exit. The musicians (insurers) struggle to perform in this chaotic environment, potentially leading to a subpar experience for everyone involved.

A well-orchestrated regulatory policy keeps the music consistent and the venue stable, ensuring a steady inflow of audience members (capital) and a high-quality performance (stable insurance market).

This analogy helps to visualize how uncertainty can quickly disrupt a formerly stable market, leading to a cascade of effects that ultimately impact all stakeholders. ###

5.5 Quantifying the Impact

While the qualitative effects of uncertainty are clear, quantifying its impact presents significant challenges due to the complex interplay of factors in insurance markets. However, several indicators can help measure the economic consequences of increased uncertainty. By tracking these metrics over time and correlating them with policy changes, researchers and policymakers can begin to quantify the economic impact of increased uncertainty in catastrophe insurance markets.

5.5.1 Insurance Penetration Rates

Definition: The percentage of properties insured against catastrophes in high-risk areas.

Measurement Approach:

· Calculate the ratio of insured properties to total properties in designated high-risk zones.

· Track changes in this ratio over time, particularly following significant policy changes or catastrophic events.

Example from Florida:

· In 2010, the insurance penetration rate for wind coverage in coastal counties was approximately 78%.

· By 2020, this rate had dropped to 72%, potentially indicating increased difficulty in obtaining or affording coverage[43].

Interpretation:

· A declining penetration rate may suggest that uncertainty is making insurance less available or affordable.

· However, care must be taken to control for other factors such as changes in risk perception or economic conditions.

5.5.2 Premium-to-Coverage Ratios

Definition: How much consumers pay for a given amount of coverage over time.

Measurement Approach:

· Calculate the average premium per $1,000 of coverage for standard policies.

· Track this ratio over time, adjusting for inflation and changes in underlying risk factors.

Example from Florida:

· In 2005, the average premium per $1,000 of coverage for a standard homeowners policy was $4.20.

· By 2020, this had increased to $6.80, an increase of 62% after adjusting for inflation[44].

Interpretation:

· A rising ratio, especially one that outpaces inflation and risk increases, may indicate that uncertainty is driving up the cost of insurance.

· This metric can help isolate the impact of uncertainty from general market trends.

5.5.3 Market Concentration Indices

Definition: Measures like the Herfindahl-Hirschman Index (HHI) to track market competitiveness.

Measurement Approach:

· Calculate the HHI by summing the squares of market shares for all firms in the market.

· Track changes in the HHI over time, with increases indicating higher market concentration.

Example from Florida:

· In 2005, the HHI for the Florida homeowners insurance market was approximately 600.

· By 2020, it had risen to 1,200, indicating a significant increase in market concentration[45].

Interpretation:

· Increasing market concentration may suggest that uncertainty is driving smaller players out of the market.

· However, this must be balanced against other factors such as economies of scale or regulatory changes that might favor larger insurers.

5.5.4 Reinsurance Costs

Definition: Changes in the cost of reinsurance as a proxy for overall market uncertainty.

Measurement Approach:

· Track the average cost of reinsurance for a standardized coverage amount.

· Compare these costs across different regions and over time.

Example from Florida:

· In 2005, the average cost of reinsurance was approximately 10% of primary insurance premiums.

· By 2020, this had increased to 25%, significantly outpacing increases in other regions[46].

Interpretation:

· Rising reinsurance costs, especially if they outpace increases in other markets, can indicate growing uncertainty.

· This metric is particularly useful as reinsurers often have a global perspective and can serve as early indicators of market trends.

5.5.5 Investment in Catastrophe Bonds

Definition: The volume and pricing of catastrophe bonds can indicate investor appetite for catastrophe risk.

Measurement Approach:

· Track the total volume of catastrophe bonds issued.